Congress is at it again, voting on yet another trillion-dollar plus spending bill. This one, titled the Build Back Better Act, is masquerading as a budget reconciliation bill just so that it can pass the Senate with a simple majority, thereby sidestepping the 60-vote threshold necessary to pass major legislation. Don’t let its name deceive you. This bill does much more demolishing than actual building, and if passed as is, will have devastating consequences for middle-class retirement savers, small businesses, innovation, job creation and, ultimately, future American prosperity.

On a recent DWealth Muse podcast, guests Matt Belcher, CEO and Co-founder of CalTier, an AltTech company that is currently democratizing access to multi-family real estate investments and Jim Jones, a Self-Directed IRA Expert who handles platform partnerships at Alto IRA, discussed some of the harsh economic repercussions of the two sections of the bill which pertain to alternative assets held in retirement accounts.

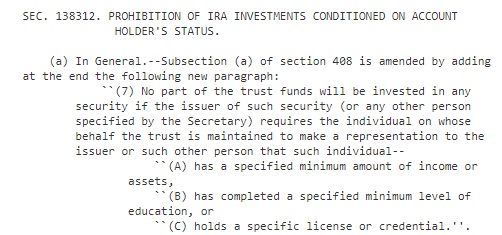

During the podcast, the AltTech experts painted an ominous picture, illustrating just how detrimental Sections 138312 and 138314 would be to middle-class retirement savers as well as to the alternative assets – such as small business funding – that the 2012 bipartisan JOBS Act was enacted to protect.

In fact, as Jones explained, this “reconciliation” bill would essentially unwind much of the economic progress made under the JOBS Act in recent years.

For those who haven’t been following, Section 138314 bans citizens from using retirement capital to invest in alternative assets as a single-member LLC, an investment strategy that is presently employed by hundreds of thousands of Americans to invest in real estate. Furthermore, Section 138312 not only halts Americans from investing their hard-earned retirement capital into many of the alternative investment products that have been proven to deliver greater risk-adjusted returns, it also forces retirement savers to liquidate many of their existing alternative holdings from their retirement portfolio.

Since there aren’t active trading markets for most alternative assets, retirement savers would, in most cases, be forced to sell their positions at a deep discount. With their funds being redirected to lesser-performing conventional investment products such as paltry yielding bonds and mega-cap publicly-traded equities whose peak growth years have long passed, it could take years for retirement portfolios to recover such losses. In fact, those who are nearing retirement age may never be able to recoup those deficits at all.

But, as explained in the podcast, retirement losses would be just the first domino to fall. Mandatory divestitures of alternative assets would lead to widespread property foreclosures and the mass collapse of small businesses, many of which have yet to recover from the covid-induced revenue shortfalls they sustained after being deemed “unessential” and forced by local governments to close. The bill’s government-imposed IRA divestitures will not only serve as the final nail in America’s small business coffin, they will set off an economic cataclysmic chain-reaction that our nation may never overcome.

In order to avoid a collapse that would put Rome to shame, U.S. lawmakers need to stop looking at these alternative assets as mere components of investment portfolios or just some numbers on a brokerage statement. Instead, they need to start recognizing them for what they truly are. They are the engine of the American economy and the very lifeblood of our society. They are the businesses that provide the healthcare benefits that keep us healthy. They are the employers who supply the wages that enable us to buy the goods from our local Mom-and-Pops and provide the tax revenue that funds our schools, our roads, our police and our fire fighters. These portfolio components are the roof over our heads, our transportation to work, and the food on our plates. They are the inventions that enhance our lives and the ingenuity that keeps mankind progressing.

And, propitiously, today, some of these portfolio components are the very blockchain innovations poised to save America’s flagging economy.

Blockchain is not just another disruptive technology. It is a foundational shift. Unlike many technologies which have preceded it, blockchain is not merely modernizing industrial processes. Rather, blockchain has formed an entirely new substratum for commerce and civilization. Blockchain’s presently unfolding transformative impact on currency and finance is not even the tip of the tip of the iceberg. Blockchain innovation has set its sights far beyond cryptocurrency.

Blockchain is already reengineering supply chains and enhancing healthcare. Soon blockchain will utterly redefine mass media. It is at the intersection of blockchain and mass media where unprecedented prosperity resides.

While not widely cited as a leading indicator of stock market growth and economic expansion, but as the chart below certainly depicts, some of the greatest bull markets in history have all coincided with innovation in mass media. In fact, throughout history, it has been a technological revolution in mass media that has rescued America from market crashes, depressions, recessions, financial meltdowns and ruptured bubbles.

The economic impact of blockchain will ultimately dwarf that of all innovation precursors combined – including the internet which, according to a recent study by the Interactive Advertising Bureau (IAB), contributed $2.45 trillion to the United States’ $21.18 trillion GDP in 2020 – an eightfold increase from 2008 – and accounted for more than 17 million of the 147.79 million American jobs in 2020.

Yet, as impressive as that is, the internet’s monumental economic impact will ultimately seem trivial in comparison to what blockchain will beget, for blockchain is the very first innovation to revolutionize mass media amid the tailwinds of a technologically progressing financial system. This is a world-defining alignment that will forever alter the planet’s economic arc.

And the smart money knows it.

According to CB Insights, during the first half of 2021 alone, over $7 billion was raised by blockchain-focused startups – far surpassing 2020’s annual total of $2.3 billion. Most of these startups utilize Regulation D to facilitate these venture rounds, a securities rule that excludes smaller investors from the same unfettered access to investment opportunities bestowed to America’s wealthier accredited investors. And like PayPal founder Peter Thiel, who turned a $2,000 IRA into a $5 billion fortune, more and more accredited investors are using self-directed IRAs to make these venture investments.

Section 138312 is apparently intended to “level the playing field” by preventing wealthier and more financially sophisticated investors from emulating Thiel’s IRA success.

However, instead of leveling it, this directive will only result in destroying the playing field altogether.

If lawmakers are truly that concerned with “equity”, there is a much more constructive solution than barring retirement capital from financing innovation and forcing premature liquidations of private businesses. Lawmakers could simply eradicate the unconstitutional accredited investor rule that discriminates investors based on net worth and, instead, grant all citizens equal access to investment opportunity.

Today’s economy – thanks, in part, to decades of discriminatory policy cloaked as equality – is way too fragile to be punishing innovators, job creators and investors of every size.