")

By: Gerelyn Terzo

After a robust first quarter in which fintech startups gripped the headlines for unprecedented VC fundraisings, the momentum continues.

Last week was no exception — including a multi-billion dollar exit for a Utah-based fintech unicorn. In addition, fintech firms are raising capital at a dizzying pace in emerging markets, while they have also moved into the conversation for one of the hottest niches in crypto — central bank digital currencies (CBDCs.)

Let’s start with the exit sign. Cloud-based software company Bill.com, which is publicly traded, announced it would acquire Utah-based accounting fintech startup Divvy in a USD 2.5 billion deal. The transaction had Wall Street analysts buzzing. Considering the complementary nature of the companies and shared focus on SMBs, Divvy has the potential to transform Bill.com and “more than double transactional revenue…on day one” of the deal, according to Piper Sandler analyst Brent Bracelin.

Divvy, which counts PayPal Ventures among its backers, has a valuation attached of between USD 1 billion-10 billion, as of early 2021 and according to Crunchbase. The fintech has been active in the VC space, attracting more than USD 417 million to its coffers across five rounds, the most recent of which was a Series D in January. Bill.com is looking to Divvy to fill a need that its customers (SMBs) have for real-time data.

Next up is a newly released report by Better Bridges and the Catalyst Fund on the State of Fintech in Emerging Markets. The companies canvassed more than 200 fintech startups and a handful of impact investors with a focus on Africa, Latin America and South Asia. Among the key takeaways are:

- Fintech investments in the emerging markets have been booming over the past half-decade, reaching USD 23 billion across the aforementioned regions. In fact, the fintech sector receives the highest level of VC investments in emerging markets, a trend that has only strengthened with the onset of the pandemic.

- The number of pre-seed and seed deals, in particular, is on the rise, though the average deal size is not consistent across jurisdictions. In Africa, the average seed round is USD 1 million compared to USD 3 million in Latin America and India.

- Payments and credit companies are attracting the most capital. In Latin America, neobanks and payments companies have been dubbed the “investor darlings” over the past half-decade.

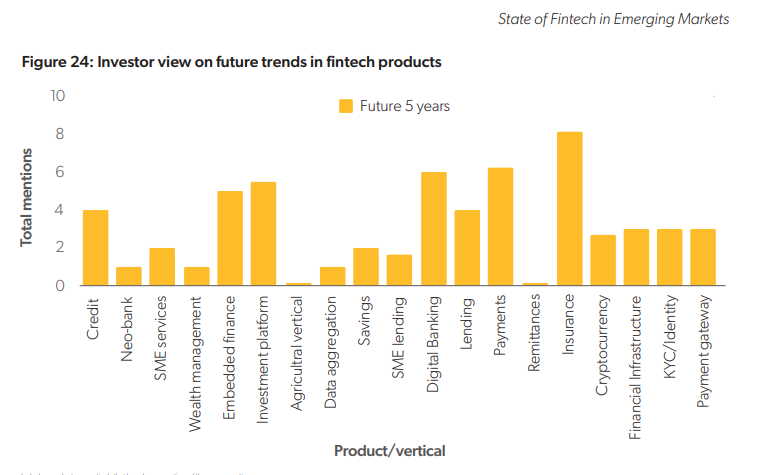

- Investors also commented on the future trends surrounding fintech products for the next five years. Most of them are excited about insurance, payments and digital banking, to name a few segments. You can see more of the results in the below chart.

Source: State of Fintech/Catalyst Fund

Meanwhile, the latest retail investor movement to scoop up battered stocks en masse in an attempt to drive up prices and leave hedge fund traders who are short the shares holding the bag is not relenting. After these Reddit-powered groups turned the tide on GameStop for a while, they are now targeting movie stock AMC.

Now a startup called Caplight, which is backed by the likes of Fin Venture Capital, Susquehanna and Clocktower Technology Ventures, is looking to revolutionize the derivatives market. Caplight gives institutional investors the opportunity to place both long and short bets on privately held companies through what the company describes as synthetic, cash-settled derivatives. Now big investors can profit from the rise or fall of a startup even if they don’t own any equity themselves, allowing them to cast a wider net with their strategies. This is an emerging trend in fintech, with fellow startup Apeira Capital similarly placing a target on the backs of startups with overly lofty valuations.

In yet another trend, global policymakers are finally waking up to the fact that cryptocurrencies aren’t going anywhere. They are trying to decide whether they want to make it difficult for the industry to continue innovating, building and investing or instead join the fray with central-bank digital currencies (CBDCs). The Economist calls CBDCs a “giant risk — but one that is worth taking.” Fintechs could help governments make CBDCs a reality.

In fact, the National Bank of Georgia (NBG), the Eurasian country’s central bank, is looking to the fintech sector in its efforts to create a CBDC. The NBG is looking to bolster the efficiency of its payments rails and create greater financial inclusion. It is launching a public-private partnership through which it is hoping fintechs, as well as tech companies and financial institutions, will help it overcome “technological, regulatory and financial issues facing CBDC adoption.”

Sticking with the cryptocurrency theme, Bloomberg’s latest Crypto Outlook report suggests that one digital currency, in particular — Ethereum — could give fintech a run for its money. According to the report, “Ethereum is to fintech and digitization what bitcoin is to gold.” Of course, bitcoin has been eating gold’s lunch, as the flagship cryptocurrency continues to steal investors away from its rival store-of-value asset — the precious metal.

According to the report, Ethereum is having a similar effect on the digitization of finance. They argue that Ethereum is best positioned to transform finance to a digital format. To be fair, the report seems to hone in on “old guard finance,” which for all intents and purposes is not really fintech. They point to the BCGI as evidence that the digitization of finance is on the rise, as the index has gained 740% since early 2020. While the index may be frothy at these levels, the Bloomberg writers declare decentralized finance (DeFi), which is largely an Ethereum phenomenon, can be “revolutionary.”

Meanwhile, talk about a more inclusive financial system, one fintech startup has taken it to another level. Employment data fintech Argyle has its sights set on gig-economy workers and is willing to put its money where its mouth is. Argyle is offering USD 500 to anyone who is willing to disclose sensitive data including their payroll account username and password. They will tack on an additional $25 USD for every month that the user participates in the program, as long as the credentials remain valid.

")

")